A strong budget is a keystone of a successful and sustainable organization. But financial planning generally remains a task executed by only a few members of an organization’s staff and board, which can lead to lack of ownership and understanding of programmatic and organizational bottom lines. On our October Distance Learning Webinar, we explored budgeting strategies that can add more staff input and investment in your organization’s financial future.

A strong budget is a keystone of a successful and sustainable organization. But financial planning generally remains a task executed by only a few members of an organization’s staff and board, which can lead to lack of ownership and understanding of programmatic and organizational bottom lines. On our October Distance Learning Webinar, we explored budgeting strategies that can add more staff input and investment in your organization’s financial future.

Our presenter for this important (and timely!) conversation was A. Michael Gellman (pictured right) — a CPA, CGMA, Senior Advisor and Former Shareholder for Rubino & Company — who has more than 30 years experience in nonprofit accounting.

His advice for better budgeting? Bring non-financial managers to the table, including key staff members. "The key word here is interaction," he said. "You want to connect managers to the budget system."

According to Gellman...

In nonprofit organizations, as in the for-profit world, it is common to think of accountants as the stewards of organizational finance. And yet, accountants do not create anything. They merely report the facts. The real stewards of organizational finance are the non-financial managers. Who are they? Non-financial managers are the people in the trenches, on the front lines and behind the scenes. They are managing programs, running organizations, directing volunteers, raising money, staging special events, writing grants, serving on Boards, managing offices and serving as interns. They are the people whose everyday actions and decisions make or break the financial health of the organization. Accounting departments, in general, operate “after the fact.” All of the decisions have been made. Accountants report the facts, point fingers, lay blame and slay the mortally wounded. It’s up to the non-financial managers to save the world.

So how do we create a better world for biking and walking by starting from within? Gellman suggests a strategy called "Behavior Based Budgeting" that turns the prevailing paradigm on its head. "Most people have it backwards," Gellman says. "It's all about how you use a budget, not how you build a budget. If you think of your budget as a tool to use daily, you will be motivated to build a better budget.

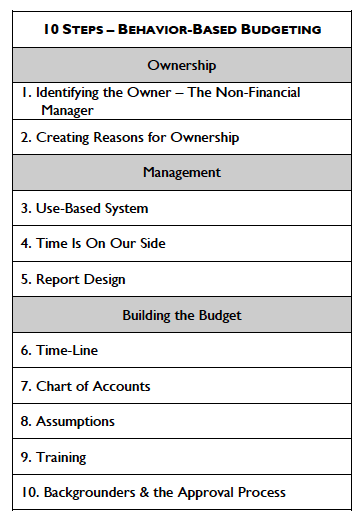

What does that mean in practice? Here are his 10 key concepts to boost your organization through more participatory budgeting.

What does that mean in practice? Here are his 10 key concepts to boost your organization through more participatory budgeting.

1) Identifying the non-financial manager as the owner of the budget process is critical. Non-financial managers are the end-users, the primary users, of the budget. The non-financial managers are not in the accounting department; they are managing the programs and operations of the organization. The non-financial managers have the most impact on the organization’s inflow and outflow of funds. The budget exists to support them in their decision-making. They are at the center of the budget process.

2) You cannot force ownership on a person. Individuals must accept ownership. We must create compelling, inherent and self-evident reasons for non-financial managers to take ownership over a process most people find unrewarding, tiresome or worse not useful. This may not happen immediately. Non-financial managers will only "buy in” to the ownership concept once they realize that a behavior-based budget can help them perform their jobs.

3) Budgets are created to be used, and used every day. Things that you use every day are essential to your existence: your car, your computer, your toothbrush, your coffeemaker. For a budget to be elevated to this “essential” status, it must provide maximum return benefits to the user. Budgets seldom do. But budgets will when they can be used to raise the awareness levels of managers and, thereby, alter their behavior. This happens when budgets are properly integrated into your organization’s management reports and paired with rolling projections, as seen below.

4) Non-financial managers must understand and believe that time is on our side. In other words, they must learn to take advantage of time, rather than making time the enemy. Identifying trends (either positive or negative) earlier in the year rather than later, creates more time to change or take advantage of that trend. Using real-time monthly budgets helps maximize budget use and effectiveness. A real-time monthly budget system breaks down each budget line into monthly segments that, as closely as possible, matches expectations of occurrence to months in the calendar. This allows you to compare a three-month actual result to a three-month budget.

5) A well-designed financial management report that brings steps 3 and 4 together literally creates the picture. If the report is designed correctly, the non-financial manager will be able to use peripheral vision to view budget, actual, historical and projected results all at once. This provides a wealth of interrelated information that directly answers the two critical questions: How am “I” doing as a manager? And how are “We” doing as an organization?

6) A well-organized and complete budget time-line keeps everybody on the same page. The budget timeline should be prepared in a chronological outline format and be completely clear in its message and purpose. Any non-financial manager who reads the outline should immediately understand its purpose and comprehend what is expected of him or her. In total, the budget outline will cover between 10 and 14 weeks from the start of the pre-planning phase through final approval.

7) Organizations seldom review their chart of accounts, departments and cost centers. During the pre-planning phase of the budget time-line, it's important to review the accounting structure. This review allows organizations to assess whether the accounting structure is evolving at the same pace as the organization.

8) Documenting "assumptions" is where most nonprofit organizations fall short. Documenting assumptions must become a priority. All of the individual line-item details within the budget must be documented. The process starts with creating a standard assumption documentation form that ensures critical details within line-items can be gathered, organized and displayed in a transparent manner. While documenting assumptions is time-consuming, assembling this information almost always leads to new ideas for cost savings and generating additional revenue. Documenting assumptions avoids the dreaded “SALY Plus 5” disease (Same As Last Year Plus 5% Increase), which perpetuates mistakes and inefficiencies and leaves no room for creativity.

9) Few organizations devote time to training staff in the budget cycle and use of the budget. Training will enhance every aspect of the budget process. Both group and individual training are important. Group training plays off the synergy of a group setting, where there is a free flow of ideas and exchange of information. Individual training is most often structured to improve and add core skills necessary in the performance of one’s job. Group trainings work perfectly at the beginning of the budget cycle, where strategies have to be aligned, resources shared and hurdles overcome. Individual training helps make sure all involved have the same basic skills and removes barriers to engagement in the budget process.

10) Organizations seldom leave time for telling the story and selling the budget. Your budget story should be a good story, but a short story. Take the time to assemble a brief budget narrative (backgrounder) for the Board that highlights changes and new initiatives and answers anticipated questions. Time spent on the backgrounder will help the approval process go more smoothly.

Learn more

Click here to watch our full webinar, which includes a detailed walk-through of an example budget to bring home many of these key concepts.

See below for additional resources by Gellman on this topic:

- Budgeting that works for non-profits

- Is your budgeting system helping to drive results?

- Creating financial expectations is healthy

Get in touch with the budgeting guru at This e-mail address is being protected from spambots. You need JavaScript enabled to view it .